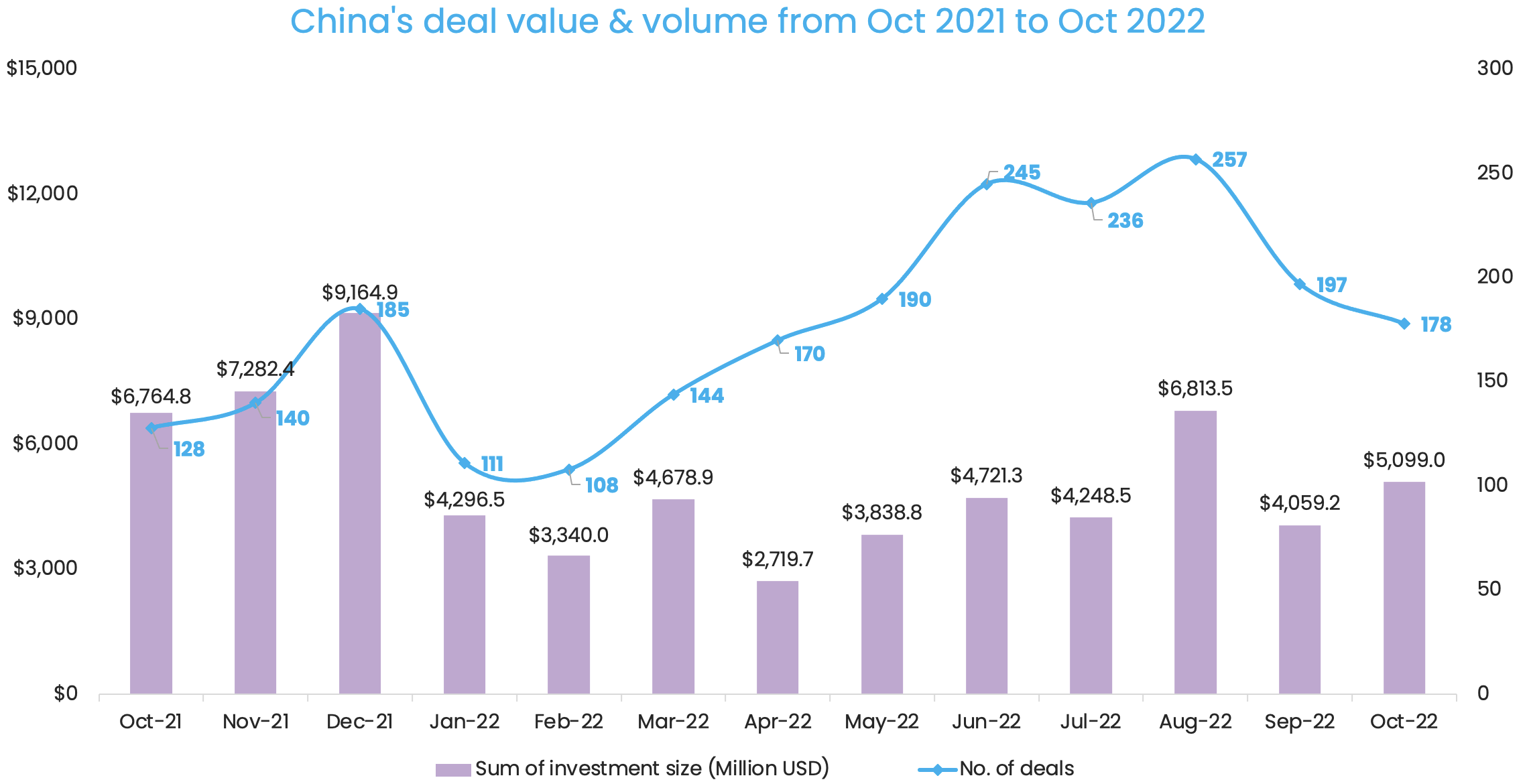

As the number of venture deals in Greater China slid further from August’s peak, October saw 178 startups raise a combined $5.1 billion. This included one megadeal that contributed almost half of the month’s total financing.

The deal count of 178 in October marked a decrease of 9.6% from the prior month. The deal value of $5.1 billion, meanwhile, was a 25.6% month-on-month (MoM) increase, according to proprietary data compiled by DealStreetAsia.

The top deal of the month was the $2.5 billion fundraising by state-linked electric vehicle (EV) startup GAC AION, which accounted for 49% of the deal value in October.

The market is cooling down from a strong third quarter. The months between July and September (Q3) had seen the completion of 690 venture deals — the highest since we started tracking the Greater China market in October 2019. Yet, the fundraising value in Q3 ($15.1 billion) failed to surpass any quarter of 2021, when large-size cheques bumped up fundraising.

Dealmaking is expected to remain active with a sustained interest in early-stage opportunities, but the level of monthly deal values is likely to stay low, or even contract. The global stock market downturn is dampening investors’ appetite for growth- and late-stage deals at much larger sizes.

As proof, the first ten months of 2022 recorded 1,836 deals that raised a combined $43.8 billion. The combined deal count was approximately 1.2 times that of the same period last year, but the fundraising value was only around 60% of that in January-October 2021.

Eco-friendly startups win large-sized cheques

A rather policy-led momentum is funnelling venture money into eco-friendly transportation, with GAC AION raising a $2.5-billion Series A round to become China’s highest-valued EV startup.

GAC AION, the five-year-old EV subsidiary of Chinese state-owned automaker Guangzhou Automobile Group (GAC), secured fresh capital from 53 strategic investors to reach a valuation of about $14.2 billion. The hundred-billion-yuan China Structural Reform Fund and state-owned power system operator China Southern Power Grid were among the lead investors. It was also one of the four megadeals in the green economy amid Beijing’s pledge to achieve carbon neutrality by 2060.

In another megadeal in October, Geely-backed commercial new energy vehicle (NEV) firm Farizon Auto closed over $300 million in a Series Pre-A round. The new financing, which was earmarked for Farizon’s product R&D and partnership expansion, was led by GLP’s private equity (PE) arm Hidden Hill Capital with participation from investors like Chinese conglomerate Transfer Group and South Korea’s Mirae Asset Financial Group.

Energy storage startup Hithium’s $277.9-million Series B round and a $137.4-million deal in Kuntian New Energy, which manufactures anode materials used in lithium-ion batteries, were the other two megadeals in sustainable development.

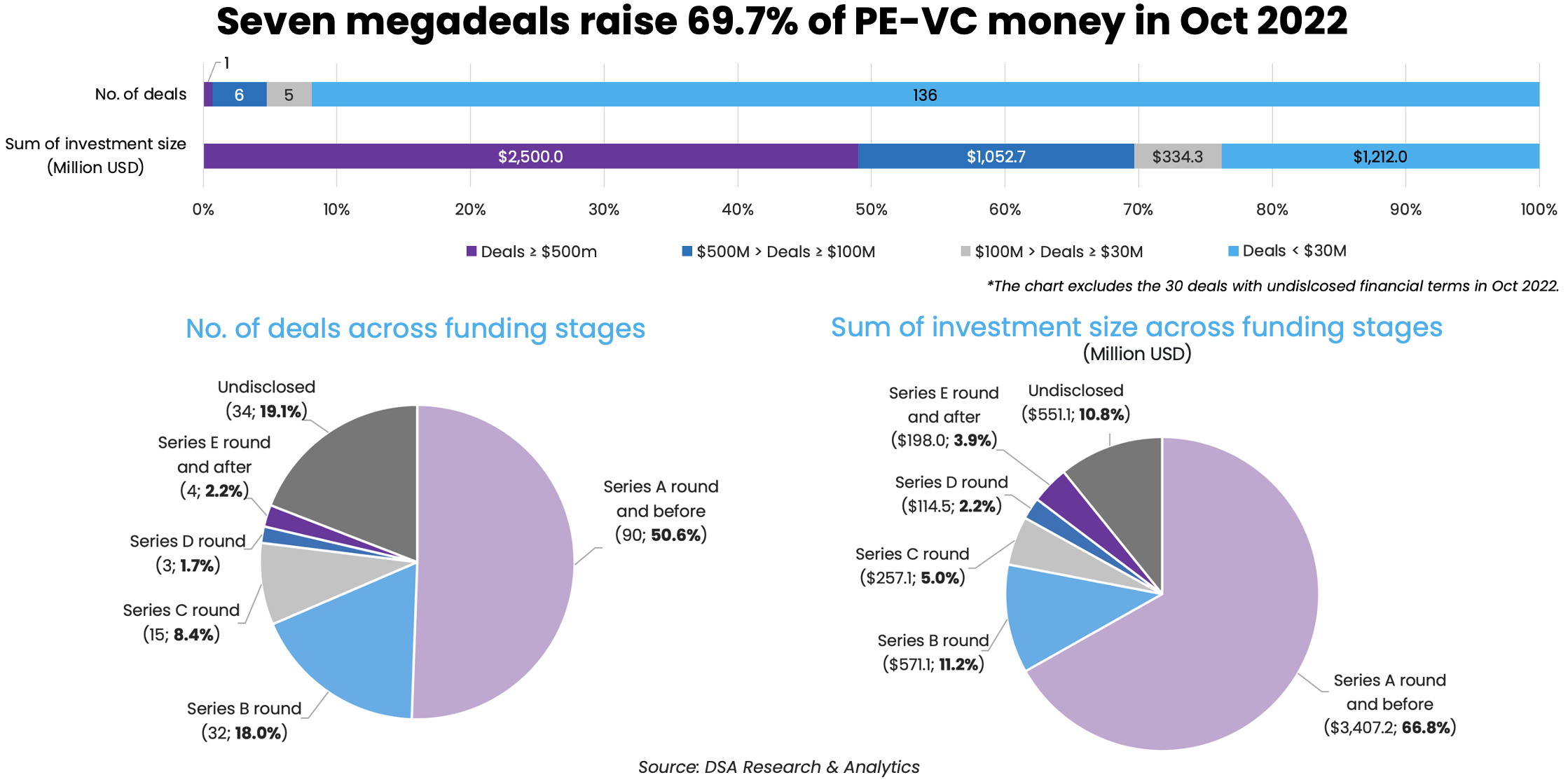

October saw the completion of seven megadeals, or investments at a size of $100 million or above. Their fundraising sum of nearly $3.6 billion accounted for 69.7% of the month’s total financing.

Investments at Series A and earlier funding stages remained dominant, with dealmaking falling sharply in companies closer to a public listing.

The 90 transactions in the earliest funding stages stood for over half of the deal count in October.

In terms of deal value, GAC AION’s $2.5-billion Series A round boosted the stage’s fundraising sum to just over $3.4 billion, or 66.8% of the month’s total financing.

In comparison, Series E and later funding stages only logged four venture deals. Facing the current economic downturn and stock market slump, investors have grown more selective with late-stage investments as they give much more priority to business fundamentals and cash runway.

List of megadeals (Oct 2022)

| Startup | Headquarters | Investment size (Million USD) | Investment stage | Lead investor(s) | Other investor(s) | Industry | Vertical |

|---|---|---|---|---|---|---|---|

| GAC AION | Guangzhou | $2,500 | A | PICC Capital, China Southern Power Grid’s investment platform, China Structural Reform Fund, Shenzhen Capital Group, Goldstone Investment (affiliated with CITIC Securities), Guangzhou Industrial Investment Fund Management | Oriental Fortune Capital, Infinite Capital Holding Company (ICAP), Yingke PE, GF Qianhe Investment, ABC Investment, BOC Asset Investment, China Orient Asset Management, and more | Auto & Parts | Electric/Hybrid Vehicles |

| Farizon Auto | Hangzhou | $300 | Pre-A | Hidden Hill Capital (affiliated with GLP) | Transfer Group, CITIC Securities Investment, Mirae Asset Financial Group, GLy Capital Management, Hunan Xiangtan Industry Fund (湖南湘潭产业基金) | Auto & Parts | Electric/Hybrid Vehicles |

| Hithium | Xiamen | $277.9 | B | ABC International (affiliated with the Agricultural Bank of China) | Matrix Partners China, Fenghe Capital, Dayone Capital, Chengtun Mining Group, Xiamen Torch Group Innovation Investment Limited Company, Xiamen Venture Capital, Goldwind | Energy Storage | N/A |

| Jiangji Distillery (affiliated with Jiangxiaobai) | Chongqing | $137.4 | Strategic Investment | Chongqing Jiangjin District Government | Consumer Products | E-Commerce | |

| Kuntian New Energy | Shijiazhuang | $137.4 | Strategic Investment | Sinopec Capital, SK China, CICC Capital | Fosun Capital, GF Qianhe Investment, Huaxu Fund (affiliated with Sany Heavy Industry) | Energy Storage | Electric/Hybrid Vehicles |

| Airwallex | Hong Kong | $100 | E2 | Square Peg, Salesforce Ventures, Sequoia Capital China, Lone Pine Capital, Hermitage Capital, 1835i Ventures, Tencent, HostPlus | Financial Services | Fintech | |

| SprintRay | Shaoxing | $100 | D | SoftBank China Venture Capital (SBCVC) | Yiheng Capital, ZWC Partners, CD Capital, Marathon Venture Partners | Healthcare Specialist | HealthTech |

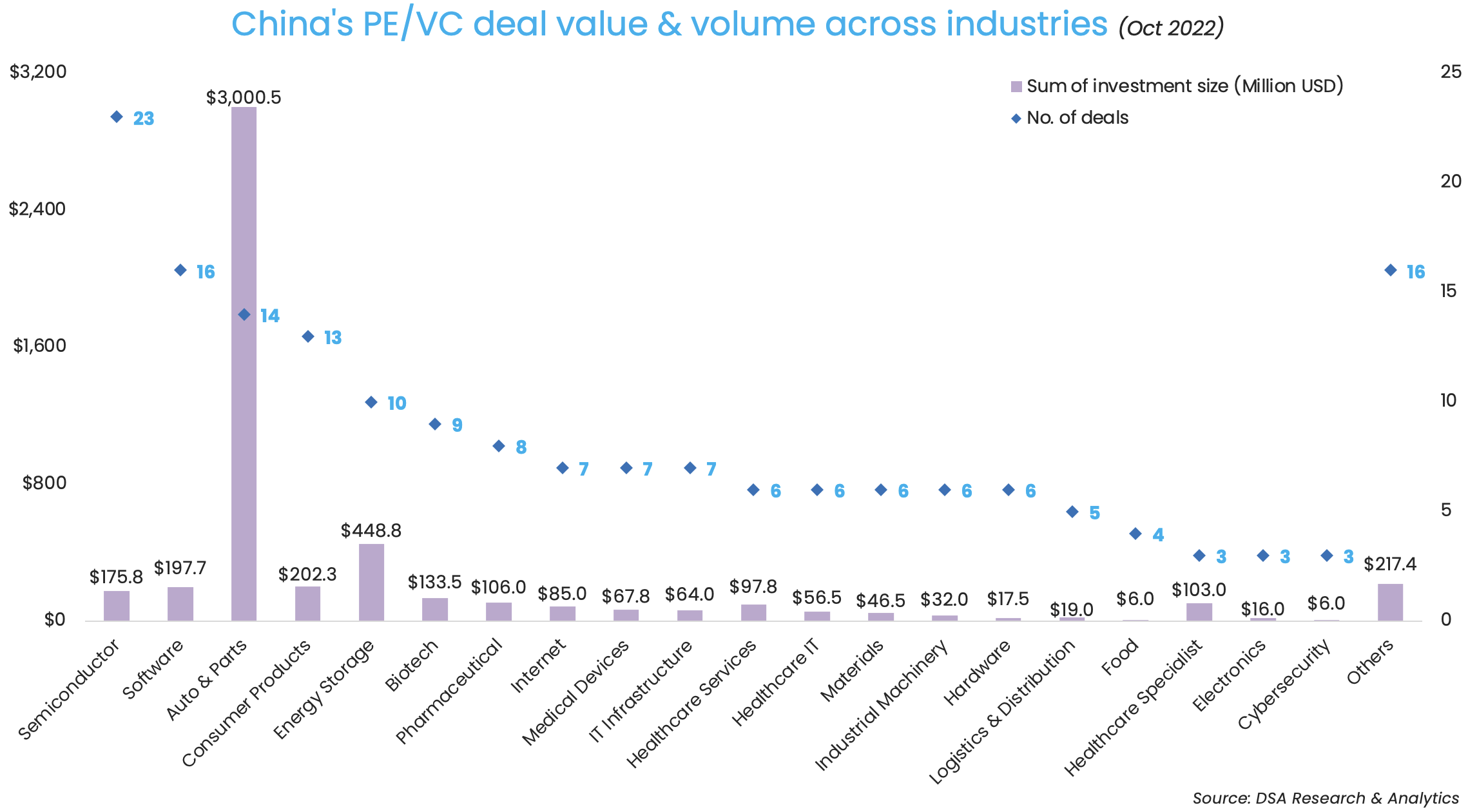

Auto & parts was Oct’s top-funded industry

The government’s efforts to develop a self-reliant, homegrown chip industry continued to prop up interest in the country’s evolving semiconductor industry, wherein startups enjoyed the completion of 23 venture deals — the most favoured sector in October.

However, megadeals were absent in the sector in the month with the biggest chip investment being a $21.8-million extension tranche in nascent chip maker Polar Bear Tech’s angel round. In total, chip startups raised $175.8 million.

The same is true for software. The sector ranked second with the completion of 16 venture deals, but their fundraising sum only amounted to $197.7 million.

With proceeds of $97.1 million, industrial software developer New Dimension Systems rose as the biggest software fundraiser with the backing of new investors including Temasek-backed Vertex Ventures and SoftBank China Venture Capital.

Thanks to GAC AION’s $2.5-billion deal, the auto & parts sector saw its fundraising total cross $3 billion to become the best-funded industry of the month. With 14 deals, the sector came third in terms of deal count.

NEV maker Farizon’s $300-million Series Pre-A round and another two mid-sized deals, namely mobility firm WESail New Energy Automotive’s $70-million Series A round and self-driving technology company EVAS Intelligence’s $41.1-million Pre-A round, also added to the fundraising traction.

State-linked, local investors move up the ladder

More state-linked, local investment companies moved up the ladder to become some of the most active investors as they answer the country’s call to aid the development of China’s homegrown technology. Their privately run, global counterparts, on the contrary, slowed down their investment pace.

Shenzhen Capital Group, Addor Capital, CITIC Securities, and State Development & Investment Group (SDIC) – all of which are backed by China’s state capital – stepped up their dealmaking efforts by writing more and, for most of them, much bigger cheques.

In contrast, Sequoia Capital China, which had always been on the winner’s podium in the previous months, just made it to the list with only three investments in October. Sequoia Capital China, the bellwether of tech investments in the region, had participated in five deals in September, following 17 in August and eight in July.

Legend Capital, a fund management unit of Chinese conglomerate Legend Holdings, was the top investor of the month with participation in 10 venture deals. Its sister company Lenovo Capital and Incubator Group injected capital into three investments.

Their combined cheques made the parent firm the most active investment group in the month, although the collective value of their deals was $163.1 million – only a fraction of the total cheque sizes seen among many other lower-ranking investors.

List of top investors (Oct 2022)

| Investment company | No. of deals | Total value of participated deals (Million USD) | Lead | Non-lead |

|---|---|---|---|---|

| Legend Holdings’ affiliates | 13 | $163.1 | 11 | 2 |

| Shenzhen Capital Group | 6 | $2,535.8 | 2 | 4 |

| Addor Capital | 6 | $45 | 5 | 1 |

| GF Qianhe Investment | 5 | $2,680.9 | 0 | 5 |

| Shunwei Capital | 5 | $61 | 1 | 4 |

| CITIC Securities and affiliates | 4 | $2,829 | 2 | 2 |

| State Development & Investment Corporation (SDIC) and affiliates | 4 | $2,626.1 | 2 | 2 |

| Matrix Partners China | 4 | $293.9 | 2 | 2 |

| Oriental Fortune Capital | 3 | $2,555.6 | 1 | 2 |

| Sequoia Capital China | 3 | $129 | 1 | 2 |

| *If one deal is backed by only two investors, we consider neither of the two investors as a lead investor. |

Stephanie Li contributed to the story.

Note: In our monthly analysis for October 2022, we have put together detailed charts of prominent deals, active investors, deal stages, and the most attractive sectors that have bagged the maximum venture dollars in the Greater China region.

Our database only considers deals officially announced by the related investee, investor(s), and/or financial advisor, while information based on market rumours and news reports citing sources is excluded.

For a more detailed analysis, and to enable comparison between primary and secondary markets, DealStreetAsia has started tracking deals of all sizes since April 2020, as against considering only transactions worth more than $10 million earlier.

We have also introduced a standardised system for industry classification. It currently includes over 50 industries, as well as over 45 new economy and high-tech verticals, which will progressively increase to adapt to local market conditions in our closely watched regions of Greater China, Southeast Asia, and India.

SE Asia Deals Barometer Report: At $1.3b, startup fundraising in Oct stays put at Sept levels

After plunging to its lowest value this year in September, fundraising by Southeast Asian startups...

India Deals Barometer Report: Startup fundraising rises 37% in Oct to $1.4b

Fundraising by Indian startups touched $1.37 billion across 87 private equity and venture capital...