Beleaguered Indonesian startup eFishery—which was deemed “commercially unviable” by financial advisor FTI in a forensic audit—floundered not only in its mainstay fish and shrimp business segments but also in its non-core financing division, particularly Kabayan financing via P2P lending.

Though financing accounted for only 1% of the startup’s $183-million revenue in 2024, it was an important link in the company’s business model as farmers, through the eFisheryKu app, could avail credit for their feed and operational costs from P2P lenders and financial institutions, thus completing the startup’s ecosystem.

Yet, FTI’s draft audit report, reviewed by DealStreetAsia, shows that Kabayan financing was a major cash drain for eFishery, accounting for a sizeable chunk of its accounts receivable (AR) and bad debt.

eFishery had entered into agreements with P2P lenders Amartha, Kredivo and Julo to provide credit to farmers with the aquaculture startup undertaking the risk in the event of borrower default.

As of Dec. 31, 2024, eFishery’s total AR stood at $68.2 million, of which nearly half, or $33.8 million, was from Kabayan financing. Moreover, 76% of Kabayan’s AR (or $25.5 million) is considered bad debt—i.e loans overdue by more than 60 days, which are deemed as unrecoverable.

Kabayan financing also accounted for half of the company’s overall bad debt of $51.5 million, indicating weak internal controls with regards to customer onboarding, according to FTI’s draft report.

Recovery challenges lead to losses

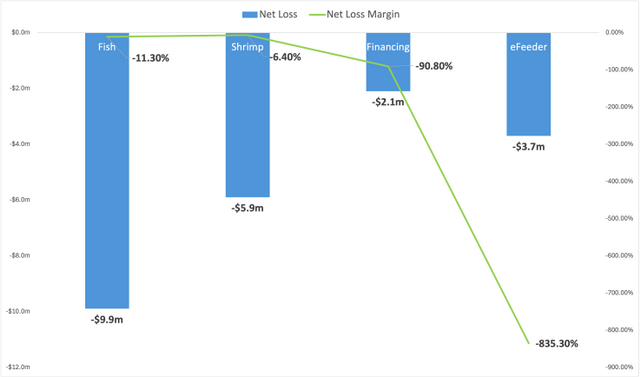

To be sure, the financing division’s net loss of $2.15 million, was much smaller than that of other segments and only a small portion of eFishery’s overall loss of almost $50 million in 2024.

It also generated a 25% gross profit margin in the year—the highest among all four business segments.

However, the financing division reported a negative EBITDA of $2.12 million and a net loss margin of 90.8%, due to high personnel costs, honorarium, outsource expenses and professional fees, shows the draft forensic report.

eFishery’s financials for 2024

“The financing provided to borrowers significantly exceeds the segment’s revenue [$2.37 million in 2024],” FTI noted.

A significant number of borrowers are located in remote areas and lack the means to repay the financing, leading to recovery challenges. Moreover, the high volume of small debtors—16,370 debtors owe less than $1,000 each—results in the cost of collection exceeding the potential recovery amount.

How Kabayan financing works

eFishery launched Kabayan in 2020 to bridge the financing gap that small farmers face. Through eFisheryKu, farmers could apply for loans to purchase feed, seeds, and inputs upfront, with repayments due after harvest.

As of Feb.1, 2025, it has processed over 150,000 transactions through various lenders, amounting to more than $87 million.

However, the fundamental issue stems from eFishery’s obligation to cover outstanding payments, even when farmers default.

According to FTI’s draft report, Kabayan operates through a structured three-party agreement involving a) lenders, i.e P2P lending platforms and financial institutions that provide loans; b) eFishery’s financing entities MTN, TUP, EAI that act as intermediaries to facilitate loan approvals and disbursements; c) borrowers, or fish and shrimp farmers, feed agents, processing companies, shrimp suppliers, etc., who avail the loans.

Farmers apply for loans through the eFisheryKu app or via the startup’s field sales agents. To assess their risk profiles, the applications undergo screening and verification by a third-party agent independent of the sales team.

Once approved, funds are disbursed but not directly to farmers. Instead, they are allocated to vendors to purchase feed and farming inputs via the eFisheryKu app, to prevent misuse (a policy introduced in 2020 after instances of funds being diverted for non-farming purposes).

While the financing model works in theory, real-world challenges persist when it comes to the recollection process. “Typically farmers say they suffered total crop failure, while others harvest successfully but use the funds for other urgent expenses,” a source requesting anonymity told DealStreetAsia.

Repayments are expected after harvest, with farmers selecting a repayment tenor of 1-6 months. However, in practice, many borrowers fail to repay on time due to crop failures, cash flow mismanagement (farmers using funds for expenses other than loan repayment), and lack of collateral enforcement (since loans are unsecured, eFishery has no legal claim over defaulters’ assets).

In some cases, farmers negotiate instalment plans, while others refuse to pay outright, leading to escalating defaults.

“At the same time, it became critical for eFishery to maintain lender confidence. When repayments slow down, P2P funders become hesitant to disburse more loans. If funding sources dry up, eFishery must work harder to secure new funding or maintain liquidity,” said the source.

A feed agent in Subang, who has partnered with eFishery since 2016 and joined Kabayan Financing in 2020, shared a mixed experience.

Initially, eFishery provided a monthly deposit of 100 million rupiah ($6,000), allowing farmers to collect feed and pay in instalments. Later, the model shifted—eFishery had to pay the agent within two weeks to a month, while extending financing to farmers for up to four months.

Consequently, payment delays began to pile up. “At first, they gave deposits, but then eFishery started falling behind on payments,” the agent said.

Despite the financial issues, the agent acknowledges the benefits that accrued from market expansion: “Our revenue grew 30-40% because of new customers. Now, they have taken matters into their own hands. If eFishery won’t pay, we’ll collect directly from the farmers.”

Concerns over eFishery’s role in loan vetting

According to FTI’s draft forensic audit report, eFishery entered into agreements with three key P2P players—Julo, Kredivo, and Amartha—to facilitate working capital loans for farmers. eFishery still has outstanding payments worth $2.6 million to the three lenders as of Feb. 1, 2025.

Meanwhile, as of Dec.31, 2024, the company has repaid all loans owed to financing institutions OCBC NISP and MTN worth around $12.7 million.

An expert on P2P lending pointed out the inherent dangers of eFishery’s field agents conducting due diligence on borrowers.

eFishery does not require a licence from Indonesia’s financial services authority (OJK) to facilitate financing for farmers since it partners with regulated P2P lending institutions, said the expert.

Yet, eFishery itself is not a financial institution, and cannot conduct due-diligence or Know Your Customer (KYC) assessments—a role that falls under the purview of licensed P2P lending institutions.

“P2P lenders cannot rely on eFishery’s customer data or claims; they must conduct their own KYC assessments to comply with regulations,” the source emphasised.

Failure to comply with OJK regulations could result in warnings for both eFishery and its P2P lending partners.

Sources told DealStreetAsia that the P2P lenders have received regulatory warnings in the past from OJK for relying solely on eFishery’s customer data instead of conducting independent verifications. “Financial literacy among small-scale farmers is low. Therefore, financial institutions and companies operating in this sector must take regulatory compliance and risk management seriously,” the sources warned.

DealStreetAsia has reached out to the three P2P players and OJK for comments.

Kredivo declined to respond, while Amartha said, “In all commercial agreements with institutions, Amartha always discusses terms and conditions that allow the company to minimise risks, aligning with its prudential principles and risk management strategies.”

“As part of its risk management framework, Amartha ensures that it conducts thorough KYC procedures, risk scoring, and eligibility assessments to verify the identity and profile of loan recipients.”

The role of LoUs

A critical component of the agreements with the three P2P players were the Letters of Undertaking (LoU)—a commitment from eFishery’s financing entities to ensure loan repayment to P2P lenders, even if borrowers default. This created a cash flow mismatch and exacerbated the cash drain.

The LoU does not serve as a full guarantee of repayment but acts as a formal assurance from eFishery’s financing entities (MTN and TUP) to lenders that obligations will be managed. In the event of borrower defaults, the LoU ensures that eFishery remains responsible for repayment coordination, which helps to mitigate lender concerns.

The terms of the LoU differ for the three P2P lenders, particularly in risk-sharing, collection processes, and repayment obligations. Julo’s LoU doesn’t require eFishery to cover unpaid loans directly, while Kredivo’s LoU explicitly states that TUP will guarantee all borrowers’ obligations. Amartha’s LoU, meanwhile, splits the risk between MTN and TUP, though it still places significant financial pressure on eFishery.

The source quoted above said eFishery’s employees acknowledged that the LoUs were necessary to maintain lender confidence, even though funders’ participation dropped from dozens to only a few.

Behind the scenes, eFishery has been settling outstanding payments to lenders, even when the farmers have not repaid the loans, while continuing its collection efforts, said the source.

“If farmers don’t pay, that means P2P loans go unpaid too. This should technically affect lenders. Instead, when a farmer is late, we ‘bypass’ the alert to prevent funders from blocking further disbursements. This allows us to maintain financing availability while we work on collections,” said the source.

“Because eFishery still focuses on a growth mindset, the company needs to grow faster,” said the source.

The use of LoUs in P2P lending raises compliance concerns under Indonesian financial regulation. Experts pointed out that OJK doesn’t allow such arrangements in P2P lending and P2P players are meant to function solely as intermediaries between borrowers and lenders.

Another industry expert from the P2P lending industry, who has previously partnered with eFishery for Kabayan financing, provided insights into regulatory compliance, risk assessment, and potential violations in the partnership model.

Other sources of cash drain

While Kabayan financing is the biggest contributor to eFishery’s cash drain, the company also faces significant financial losses from high operating expenses ($28.87 million) and inefficient technology development ($8.5 million), according to the FTI audit report.

At its peak in January 2024, eFishery had 2,599 employees, many of whom were engaged in manual labour due to the underdeveloped technology. The company’s personnel expenses alone amounted to $28.87 million in 2024, driven by the need for a large workforce to serve farmers across Indonesia.

Other fixed costs, such as rent, logistics, and overheads, further added to the financial burden.

Despite raising $314 million in equity financing over five funding rounds, only $8.5 million (2.7%) was allocated to technology development. The low adoption of eFeeders (only 6,300 deployed) and the lack of integration with sensing devices rendered the technology ineffective, forcing eFishery to rely on manual labour, according to the FTI report.

This inefficiency increased costs and reduced operational effectiveness, further contributing to the cash drain.

“eFishery is essentially operating as a supplier of feed, non-feed items, and fingerlings to farmers in the upstream cycle and as a trader of both fish and shrimps at the downstream cycle. Both of which are traditional businesses that are labour intensive and low yield,” stated FTI in the report.

The report suggests that bulk of eFishery’s business should be shut down and its intellectual property monetised or spun off. Following this, investors could recoup up to $42.7 million from liquidating Indonesian assets under the most optimistic scenario. This would come from assets, including cash reserves and short-term investments, at the Indonesian entities. That is just under 10 cents for every dollar invested.

Meanwhile former CEO Gibran Huzaifah and former chief product officer (CPO) Chrisna Aditya Wardani are alleged to have violated Singapore’s Companies Act, and there are plans to file a new police report in the city-state against the co-founders and former directors of eFishery, according to documents seen by DealStreetAsia, adding to similar filings in Indonesia.