Indian startups ended the year with funding proceeds worth $1.38 billion in December, down 17% from $1.66 billion in November, according to proprietary data compiled by DealStreetAsia. At 98, however, the volume of venture capital (VC) and private equity (PE) transactions was up 19% from November’s tally of 91 deals.

The values of 10 deals were undisclosed during the month, the data showed.

On a year-on-year basis, the total deal value in the month increased 28% over December 2023 when startups closed deals worth $1.08 billion through 71 transactions.

While fundraising by Indian startups began on a tepid note in 2024, it stayed upwards of $1 billion for the most part of the year, particularly in the second half. Investments last year peaked in June when startups scooped up $2.24 billion from 94 transactions.

Startup fundraising in India in 2024

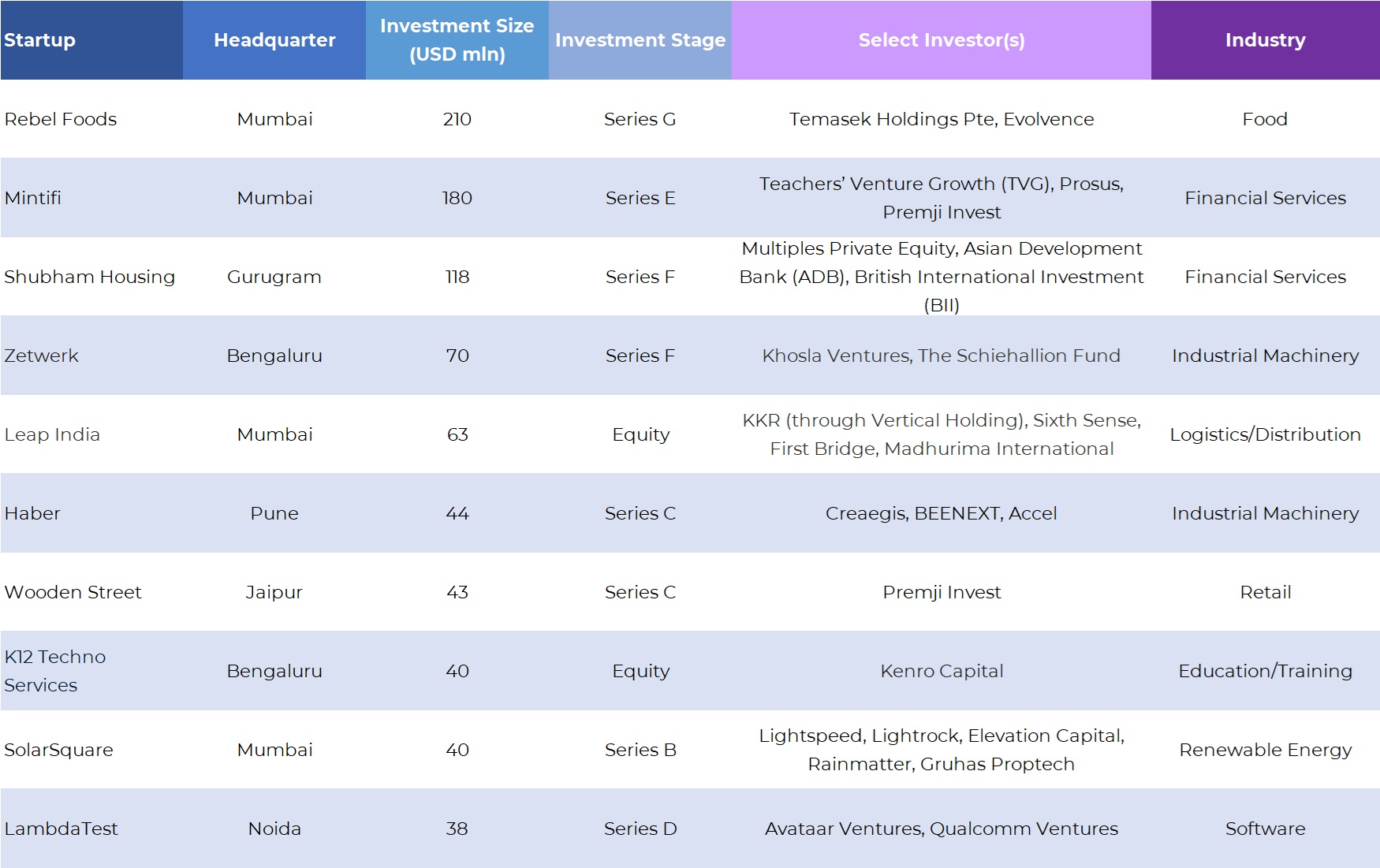

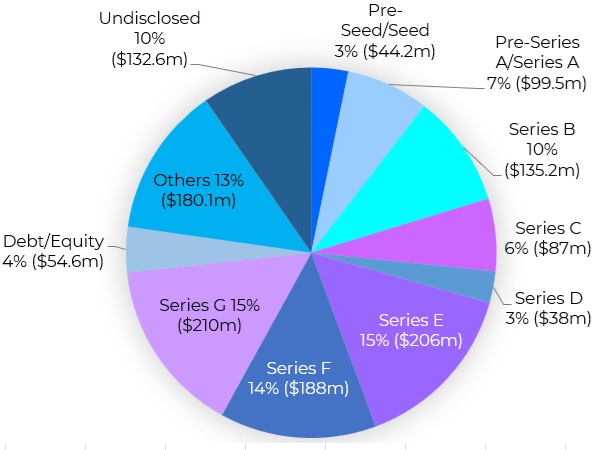

In December, there were three deals where the funding size crossed $100 million, also referred to as megadeals. Among them, Rebel Foods raised the largest round of $210 million in Series G funding led by Singapore’s Temasek Holdings Pte, with participation from existing investor Evolvence. The funding announcement came as a precursor to the company’s plan of launching an initial public offering (IPO) by 2026, per a Bloomberg report. The investment reportedly valued the Mumbai-based company at $1.4 billion.

Rebel Foods currently operates over 45 brands and 450 kitchens globally across multiple countries, including India, the UAE (Dubai, Abu Dhabi, Sharjah), UK, and Saudi Arabia. Its brands include Faasos, Oven Story, Behrouz Biryani, Mandarin Oak, The Good Bowl, SLAY Coffee, Sweet Truth, Wendy’s, and more.

Top 10 funding deals in Dec 2024

The other prominent deal during the month was closed by supply-chain financing startup Mintifi, which raised $180 million in its Series E funding round co-led by Teachers’ Venture Growth and Prosus. The round was also joined by Premji Invest.

Shubham Housing Development Finance followed with a $118-million fundraise in a round led by Multiples Private Equity. Existing investors Asian Development Bank (ADB) and British International Investment (BII) also participated in the round.

Other notable deals announced in the month include contract manufacturing startup Zetwerk ($70 million), logistics solution startup Leap India ($63 million), AI-based robotics startup Haber ($44 million), omnichannel furniture brand Wooden Street ($43 million), education startup K12 Techno Services ($40 million), rooftop solar startup SolarSquare ($40 million), and cloud-based testing platform LambdaTest ($38 million).

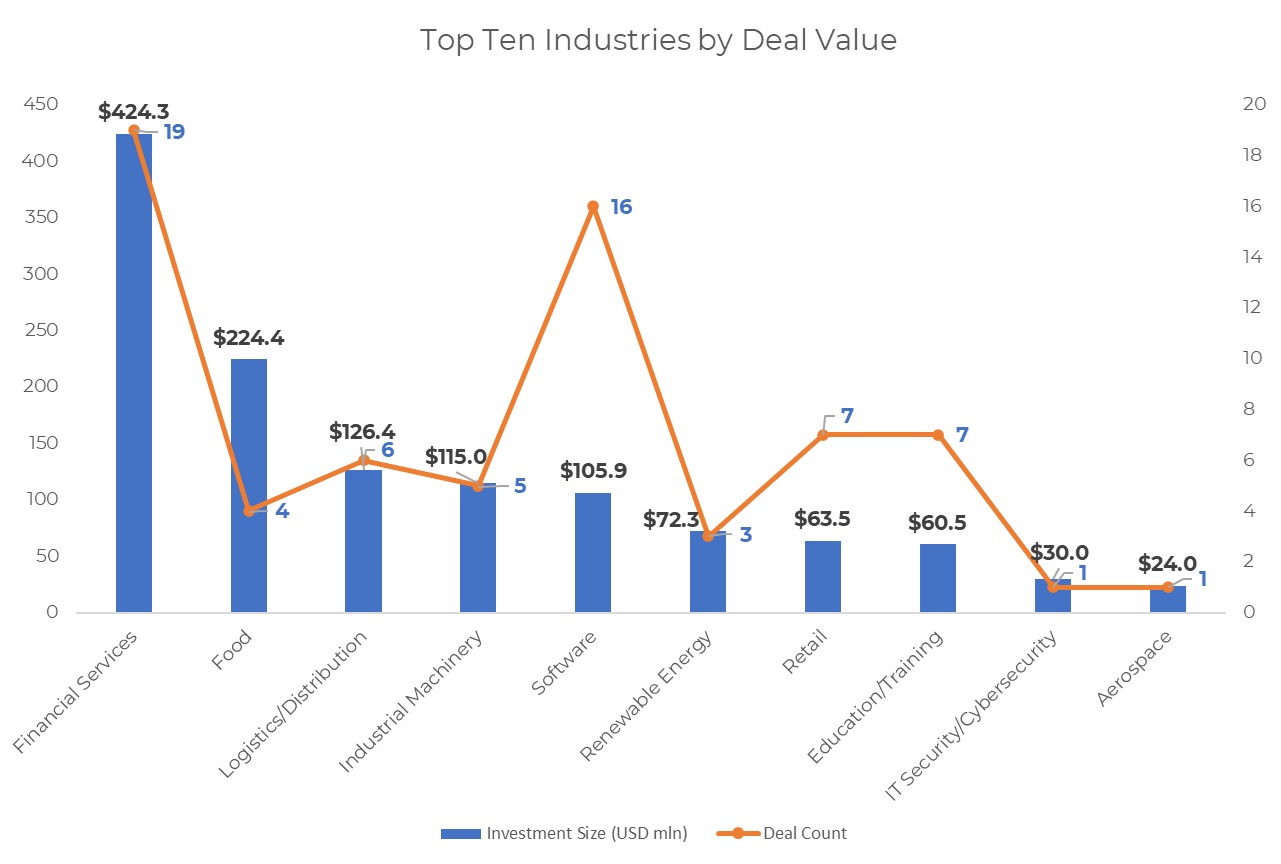

Financial services makes it to the top again

Financial services was the most funded industry in terms of both deal value and volume in December with a total of $424.3 million raised across 19 deals. This is almost thrice the amount raised by the industry in November.

Within financial services, Mintifi bagged the largest round of $180 million. Other financing deals in the month include Shubham Housing ($118 million), OneCard ($25.5 million), Snapmint ($18 million), Veefin Group of Companies ($16 million), Varthana ($15 million), Avanti Finance ($14.2 million), Svakarma Finance ($10.4 million), and Univest ($10 million).

Rebel Foods’s $210-million round pushed the food industry to the second spot with funding proceeds worth $224.4 million from four deals. During the month, the Mumbai-based foodtech firm also received an undisclosed amount from global investment firm KKR.

The other two transactions within the industry include Captain Fresh ($12 million) and WickedGud ($2.36 million).

At $126.4 million, logistics and distribution was the third most funded industry. The amount was raised across six deals including Leap India ($63 million), Instant-XP ($35 million), Shiprocket ($26 million), Fitsol ($1 million), CargoFL ($786,713) and VOICE ($588,235).

Together the top three industries —financial services, food and logistics and distribution — raised a total of $775 million, accounting for 56% of the deal value in December.

Growth-stage deals take a hit

Companies in the Series B or post-Series B rounds (including pre-IPO and private equity rounds) collected an aggregate of $911 million through 18 investments in December compared with an aggregate of $1.24 billion raised last month across 11 transactions. The share of growth-stage deals in total funding also dropped to 66% in the month from 75% in November.

One pre-IPO round was closed during the month, while two private equity transactions worth $35 million were announced in December.

Growth rounds in December were raised by LambdaTest ($38-million Series D), Rebel Foods ($210-million Series G), Shubham Housing ($118-million Series F), Zetwerk ($70-million Series F), Mintifi ($180-million Series E), Shiprocket ($26-million Series E), Haber ($44-million Series C), Wooden Street ($43-million Series C), Avanti Finance ($14.2-million Series B), Bizom ($12-million Series B), and Pixxel ($24-million Series B), among others.

Early-stage deals, comprising seed to Series A deals, were also subdued during the month. However, pre-seed and seed-stage funding almost doubled to $44.2 million from November. The largest seed round of $8 million was raised by FirstClub Technology, a member-only retail platform, from Accel & RTP Global.

Other seed transactions closed in the month include FinX ($6 million), East Ocyon Bio ($4.2 million), Sparkl Edventure ($4 million), Confido Health ($3 million), Zfunds ($3 million), Culture Circle ($2 million), Quanfluence ($2 million), Mili ($2 million), and Curie Money ($1.2 million).

Meanwhile, investments raised by startups at the pre-Series A and Series A stages were down to $99.5 million across 20 deals from $213.7 million across 32 deals in November. Enterpret, an AI-enabled customer feedback intelligence platform, led Series A funding with $20.8 million spearheaded by Canaan Partners, a US-based venture capital firm.

Deals involving debt and a mix of debt and equity raised a total of $54.6 million from five deals.

Top investors

Venture capital firm YourNest emerged as the top investor in December with at least six investments, including Superfone, a business phone and CRM app for SMBs; Leanworx, a startup specialising in real-time data for manufacturing plants; Induz, a startup specialising in data security and confidential computing; ThinkMetal, a maker of desktop 3D printers; Presage Insights, a cloud-based AI predictive maintenance and asset monitoring software; and CargoFL, a B2B technology ecosystem for logistics.

Venture Catalysts, along with its accelerator fund 100Unicorns; Accel; and Inflection Point Ventures (IPV) occupied the second place with four investments each. Accel invested in startups including Haber, FirstClub Technology, RapidCanvas, and Orange Health Labs. IPV’s investments include SustVest, Neuranics, MBG Card, and Navanc, while Ventures Catalysts invested in SustVest, The Money Club, and Power Gummies.

Meanwhile, Blume Ventures along with its founders fund Elevation Capital; Lightspeed; and Peak XV Partners made at least three investments each.

Greater China Deals Barometer Report: EV frenzy drums up Dec funding activity

Private equity and venture capital investors raced to wrap up 2024 with more signed term sheets, as dealmaking activity rebounded to record highs in December.

SE Asia Deals Barometer Report: Startup funding surges in Dec as megadeals resurface

Startup fundraising in Southeast Asia dropped to a seven-month low in November, according to proprietary data compiled by DealStreetAsia, highlighting a continued tightening investment environment for privately held companies across the region.