Partner content in association with

What will it take for insurance to be a great investment opportunity for Asian PE firms?

Photo by Vlad Deep on Unsplash

- Insurance is in the top 3 categories for private capital investments, beating FMCG and real estate

- It’s viewed as a viable investment opportunity going forward, with nearly 61% of respondents to a recent DealStreetAsia survey seeing themselves being involved in a transaction in the space over the next year.

- Strong growth prospects and the embrace of digitalisation by the industry are among the top factors that contribute to insurance being a compelling investment.

These are some of the topline findings of a recent survey conducted by DealStreetAsia to gauge investor interest in the insurance sector. The survey was sponsored by Milliman, an actuarial and consulting firm. Milliman has been involved in more than three-quarters of the major M&A transactions in the industry over the past decade, representing more than USD $100 billion

The research project was inspired by a truly marquee year for investments in the insurance sector from the private equity industry, particularly in the United States. Via the survey, DealStreetAsia attempted to discover how its audience of private capital investors and dealmakers in Asia viewed the insurance space, and if a similar glut of investments was likely in this region as well.

On the verge of booming: Investor interest grows in the insurance space

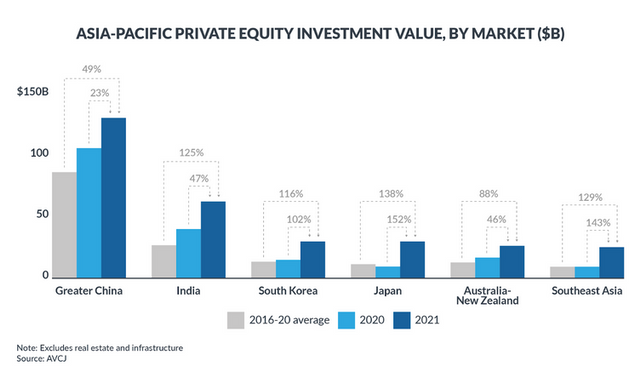

Private equity investments over the last five years have made the Southeast Asia (SEA) market one of the fastest growing regions in the Asia-Pacific region, according to Bain & Company’s 2022 Private Equity Report. And according to DealStreetAsia data, 2021 has been a record-breaking year for private capital investments, with startups in SEA and India raising $25.7 billion and $46 billion respectively.

In the United States (US), private capital flooded into the insurance sector. By mid 2021, the sector had accounted for $12.1 billion in deals, comfortably eclipsing the previous record of $9.7 billion from 2018, according to data from Refinitiv. A McKinsey report from earlier this year stated that private investors “announced deals to acquire or reinsure more than $200 billion of liabilities in the US.” Such investors currently own over $900 billion of life and annuity assets in Western Europe and North America. When all pending deals close, private investors will own $620 billion of the market – representing a 12% ownership of life and annuity assets in the US.

The same report found that the five largest private equity (PE) firms (by assets), have significant holdings in life insurance, representing at least 15% and up to 50% of their total assets under management (AUM). Insurance firms represent a form of “permanent capital”. This is derived from the assets in the balance sheets of life and annuities companies, which are available to be invested, until the demand for a payout is made. The report said, “The cost of servicing liabilities is significantly lower than the potential investment return. The spread represents an attractive margin.”

Insurance as an investment opportunity in Asia

The Asian market is poised for growth, with a large emerging middle class that is expected to increase consumer spending in the region. Throughout the course of last year and early this year, private capital investors in Asia have been warming up to the various opportunities within insurance. The market pressures of COVID-19 accelerated digital transformation in the sector, resulting in a shifting landscape. This has increased the attractiveness of insurance investments. PE firm KKR which manages $470 billion globally, with $6 billion in India, recently announced its acquisition of a 9.9% stake at a reported Rs 1,800 crore (approx. $23.4 million) in India-based insurance firm Shriram General Insurance.

It’s not just traditional insurance businesses that are drawing investors in. Within the space, insurtech is emerging as a category apart from the more familiar and established life, health, and general insurance. Insurtech refers to a multiplicity of business models including but not restricted to the digitalisation of traditional insurance firms. It allows companies to reach a far wider audience, including sections of the population that are un-or under-insured. It represents a fundraising opportunity for companies that can tap into pre-existing investor interest in both insurance as well as technology driven solutions.

Insurtech has gained ground as a vertical within the overarching fintech space. Investments in fintech accounted for US$25.7 billion in Southeast Asia — the single largest sector when it came to private capital fundraising in 2021. Insurtech made it to the top five verticals within fintech in Southeast Asia for 2021, according to data from DealStreetAsia, raising $357 million over 21 deals.

To more accurately capture insights into insurance as an investable opportunity, DealStreetAsia conducted a survey with respondents from the worlds of private capital investing, investment banking, asset management, and equity research.

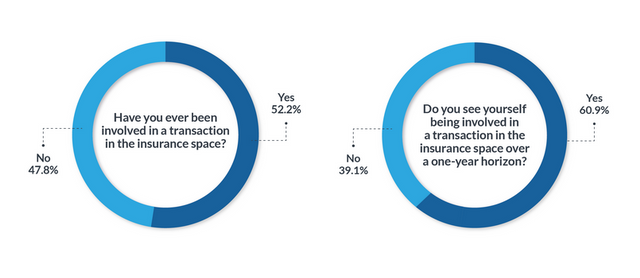

Over half of the respondents (52.2%) had previously been involved in a transaction in the insurance space. However a larger number (60.9%) saw themselves being involved in an insurance related transaction over the next 12 months, demonstrating an increasing interest in the sector.

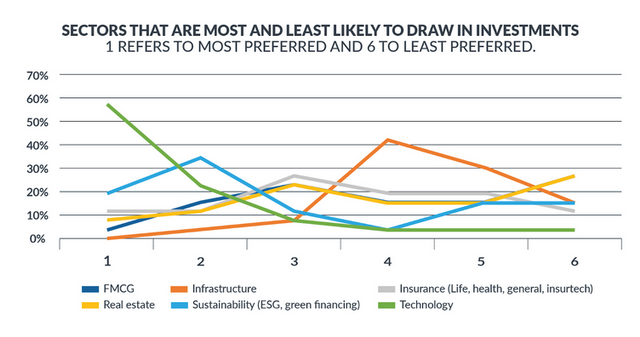

Technology and sustainability (ESG & green financing) emerged at the top two spots. However insurance took the third place, ahead of infrastructure, real estate and FMCG.

This comes as no surprise. For the tenth year in a row, ‘Internet and Technology’ garnered the largest share of capital, accounting for 48% of the overall Asia Pacific deal activity by value (Bain & Company, 2022).

Further, Bain & Company’s Private Equity Report 2022 stated, “The increase in ESG regulations across the region has created a significant investor focus on companies with products and services linked to the environment, renewable energies, and clean technologies. More than 95% of private equity investors plan to increase their focus on ESG-related issues in the coming three to five years, encouraged by investor demand, according to our 2022 Asia-Pacific GP survey.”

This shines a light on the untapped opportunities for insurance companies. To improve their appeal to PE firms, they should:

- Innovate and update their business models

- Invest in insurtech

- Develop and execute strong ESG strategies and initiatives with transparent reporting

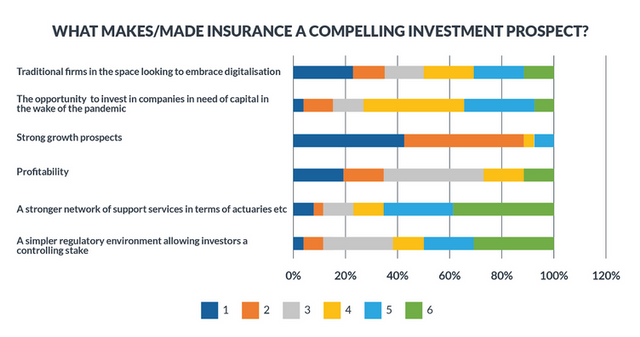

Insurance can be a compelling investment prospect. The DSA survey analysed the top reasons investors chose insurance deals, with ‘strong growth prospects’ having the largest appeal. ‘Traditional firms embracing digitalisation’ and ‘profitability’ were among the other top reasons:

This indicates that PE firms are likely to make investment decisions based on:

- Progression towards digital transformation

- Favourable economic conditions that are likely to increase growth and profitability of insurance companies

- A healthy balance sheet that provides a low-risk investment

- The expected return on investment (ROI)

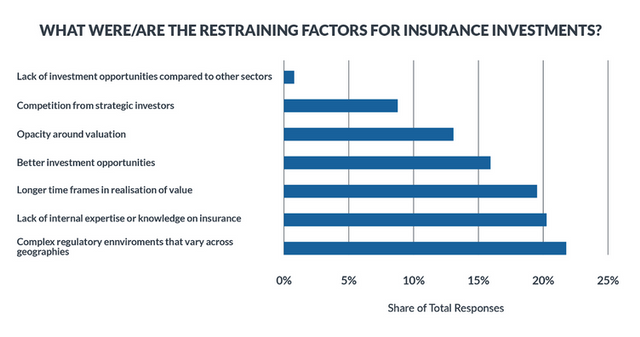

Presently there are still perceived barriers to investment. The survey looked at restraining factors for investments into the insurance space, with the top three issues being:

- A complex regulatory environment that varies across geographies

- Lack of internal expertise/knowledge on insurance

- Longer time frames in realisation of value

The survey results show that both governments and firms within the industry have their work cut out to increase capital inflow into the insurance sector. Creating clear operating structures and localisation strategies to work across different regions will support the growth of insurance firms. It will help them provide transparency to investors about risk management and ROI, despite regulations differing across regions. Education proves to be another opportunity for insurance firms. Working with industry and PE investors to understand the nature of the business could increase awareness and attractiveness of the opportunity. Lastly, an insurance firm needs to have clear value creation, to ensure its competitiveness, success and secure a return for PE firms.

Methodology

The results of the research were based on a survey administered to the readers of DealStreetAsia. For the survey, 46 responses were considered. The largest proportion of respondents came from business consulting and investment banking; venture capital, and private equity.

References:

https://www.bain.com/insights/asia-pacific-private-equity-report-2022/

This survey was conducted by DealStreetAsia and sponsored by actuarial and consulting firm Milliman. Please visit the official website for more information on its services and how Milliman can help you with valuations, market entry, strategic advice, and a better understanding of M&A in the insurance space.